More than food (… and beer)

We cannot not eat. Do we need COVID to remind us of this?

A crisis is an opportunity. In this case, an opportunity to reflect on the impact of disruptive events on the South African food system. The text below is not in any way a complete overview of the South African food system. It aims to highlight:

- Our dual economy: The need to think about the impact of food insecurity on the poor.

- Technology: The role of technology in improving efficiencies, but also to cause social inefficiencies.

- … and lastly our relationship with beer.

Let us look at the food landscape and what role technology plays, could and should play in addressing this problem.

Food security

Firstly food security. Three concepts underpin food security; access to food sources, affordability and food safety. These are the “first-tier” components of a food system that builds food security. The fact that a country produces agricultural products does not mean it is food secure. Consumers also need to be able to afford food. Large scale agricultural products might be produced in a country, but if the production is not complemented by a broader nutritional basket, it weakens food security. So food security is not just about production; it is also about nutritional security – producing the right types of product. When one looks at food systems using a nutritional approach, a completely different picture emerges of countries that are deemed food secure like South Africa.

South Africa is not food secure

South Africa is a food secure country only on paper. We do produce more than we can consume. With world-class growers, excellent infrastructure and effective marketing channels, South Africa should not have a single person malnourished, especially children. We are one of the few countries that can produce fresh staples (most vegetables) all year round!

However, the reality is that currently, around 30 million people are food insecure in this country. Before COVID-19 South Africa already had a food security crisis (Du Plessis, 2020). Chances of a child dying in South Africa of malnutrition is 37 times that of the risk that COVID-19 poses (COVID-19, 2020).

Food consumption in South Africa has always been a bit of an anomaly:

- 1 in 6 households struggles to get enough food

- 1 in 4 are hungry most of the year

- 25% live below the food poverty line (StatsSa, 2019)

The above does not only have an impact on hunger per se but malnourishment which forms the real danger in food security (stunted growth in children is 26% in the under 5-year-old category, for example). To think that the only food some children receive daily is from schools or feeding schemes, is a point of deep reflection. Compounding this aspect is that hunger and malnourishment lead to poor health and learning, affecting productivity and strain on social services. In turn, it reduces productivity and joblessness, a vicious cycle.

Given the fact that we need to increase our local food production by 50% by 2050 in order to feed an estimated 73 million people, this problem requires us to re-look at what we produce, how we produce it, how we market it and sell agricultural products. Even if there is large scale production, growing the right type of product to supplement a healthy diet also needs to occur. If we are currently not feeding the population, how are we going to do things differently in 2050?

Typically the approach is to focus on primary production as the solution. Let us just produce more. Improved technology in seed, fertiliser, irrigation techniques, mechanisation etc. has led to higher yields and also been successful in getting emerging growers to improve production output.

But where do they sell the product? To whom? Given the highly formalised supply chains, the ability of a small grower to competitively take part is impaired, pushing them back into cooperating under a co-operation agreement that ultimately makes them glorified out-growers and price takers. So the production is there, what now?

“We need to worry about the distribution of food and access to food.” (Pierri, 2019)

The focus needs to shift up the chain. It is not just about technology (like QR codes, AI, Apps etc.), it is about the alignment (I always struggle with this word), of the technology with the physical nature of especially post-harvest perishable product value chains. An alignment that requires a deliberate broad view of the value chain, inclusive of micro relationships, informal norms and low levels of trust. How to coordinate the stakeholders into such a configuration? It is this aspect that is posing a challenge.

Value chains are only of value if they unlock value to the participants.

A fragile parallel food system

If COVID-19 did highlight a weakness in South Africa’s food system, then it is how fragile this food system is. With all the technological advances up and down the supply chain, we have made our local (and global) supply chains very efficient, but also extremely vulnerable to short term shocks (very visible shocks). In parallel to this, South Africa feeds millions of people via an extensive social net and informal trade sector (not as visible). We have fine-tuned and exploited costs and convenience to such an extent, that even the slightest disruption causes major panic amongst businesses and consumers.

The short disruptions in trade on the various markets due to COVID-19 had an immediate response from affected groups. People could not eat. Informal trade immediately placed pressure on the government to open markets and allow trade within one day of potential closures. Informal buyers on the markets service extensive distribution networks into the surrounding low-cost housing areas. The impact of these disruptions hit these poorest the hardest.

Those that are day and weekly wage earners, typically also purchase food for daily consumption. Lack of storage, travel in cramped taxi’s, low disposable income, crowded living conditions etc. all contribute to the inability to store food.

Returning to older times, where basic food was produced around the house/plot (some vegetables, maybe a cow, some chickens/eggs). If not around the house, then close to the community/town. What looked like an inefficient fragmented supply chain, is ironically a more food secure option.

I recall the tale of a farmer just outside of Bloemfontein. He lamented that he is producing pre-pack sweet corn and have to send it to the Tshwane market because there are no bulk buyers locally, only to see his product for sale back on the shelves of a retailer in Bloemfontein.

This type situation becomes even more pronounced when looking at global supply chains, where food distribution planning is driven by an industrialised approach. In the end, only those products that offer economies of scale are seen as profitable. Fewer products are ultimately produced, at lower prices, shipped globally, consumed in super processed form, a significant degree ends up wasted and to top it all, making us sick through reduced nutritional value.

Reflecting on food systems, we are at a tipping point where efficiency gains are negatively affecting the social benefit. The food system and natural system have decoupled.

Lastly, what about the environment?

The industrialised scale of agriculture has had a severe impact on the planet. If one looks at our consumption of meat products, the contribution to global warming is far more significant than that of the transport sector. Once one unpacks the value chain linkages, that is from the production of meat, the cultivation of feed, the pressure on land and deforestation, manufacturing of pharmaceutical products and fertilisers, the real impact becomes clear.

A more “inefficient” model as we had in the distant past was a more balanced and sustainable solution. And then we have not touched on the employment impact of automated agricultural practices.

How do we look at how technology could and should be utilised? What should our approach be?

Some pointers:

– Understand that the “problem” exists in a techno-social-political dimension.

– Smart thinking is required, not just smart technology.

– Informal trade does not imply unsophisticated or not valuable.

Food systems are interconnected and deeply embedded in their communities. Our interventions should reflect this.

To beer or not to beer (Shakesbeer)

Lastly, lastly, time for a beer.

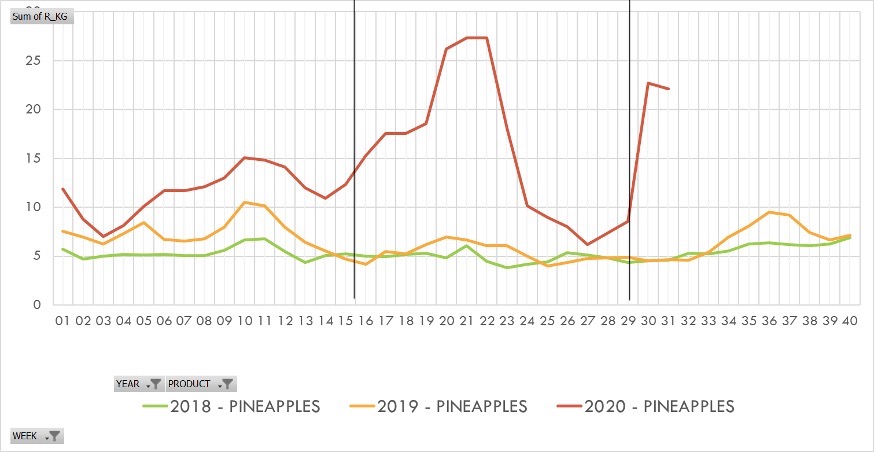

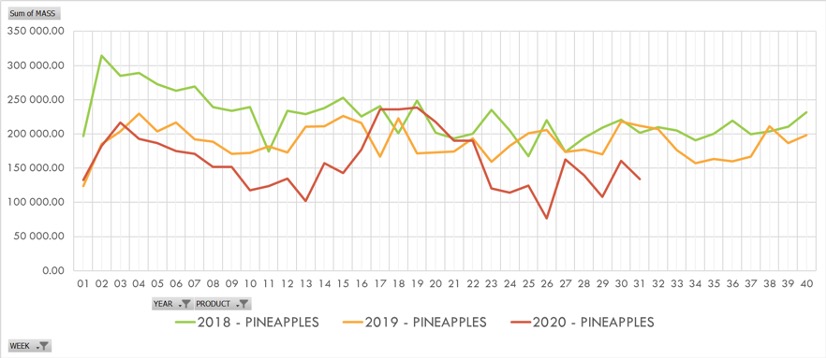

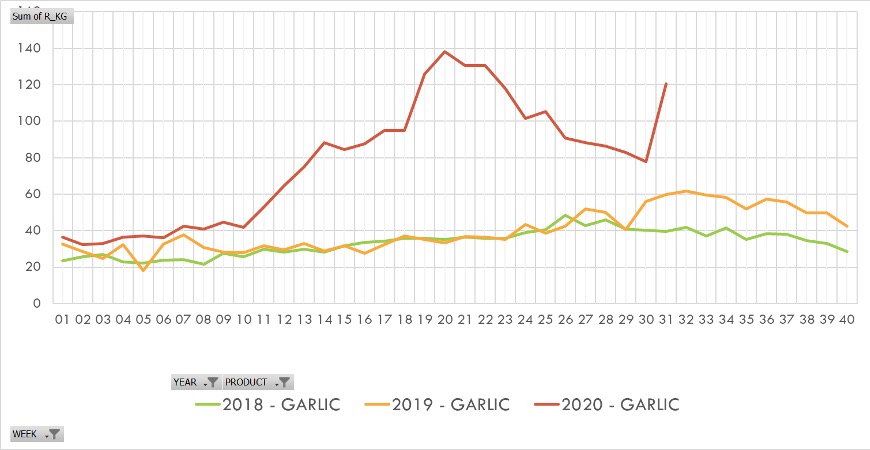

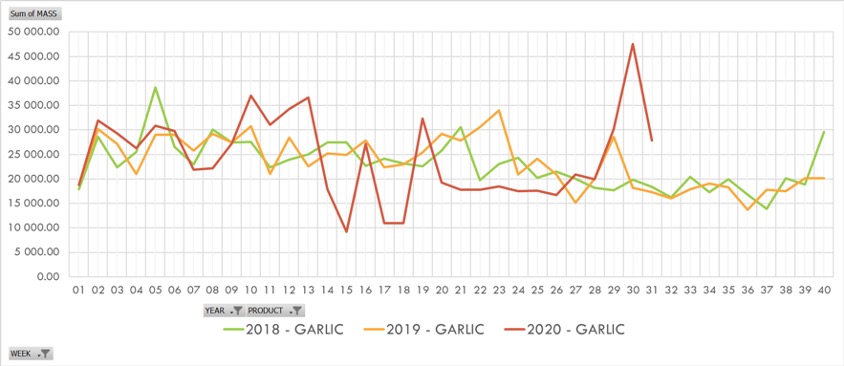

This section will share some of the price fluctuations of fresh vegetables and fruit in South Africa. During week 14/15, beginning of COVID-19 measures in South Africa, prices fluctuated substantially, and for two weeks markets could not price in the real value of sales volumes. They were even sparking the Competition Commission to launch an investigation into the price movements. The graphs below illustrate the weekly prices for certain products over three years (2018, 2019, 2020 – weeks 1 – 40) of the Johannesburg fresh produce market in City Deep. They illustrate the mass sold and price per kilogram. The same graphs were used as a response to the Competition Commission’s investigation to demonstrate the free-flowing self-correcting nature of the market system.

Important to note the following points:

– There is a Rand per kilogram graph and a mass graph. Look at them together as mass is an essential driver of price.

– The RED line represents the 2020 calendar year.

Apart from the period around week 14 when the virus measures were introduced, most of the commodity lines went back to normal fluctuations in mass and price. This indicates the strength and resilience that the fresh produce sector has in South Africa. This sector feeds the formal as well as the informal sector. If it were not for this sector, food security would have been significantly worst in South Africa.

Pineapples

Pineapples became a complete anomaly. The resourcefulness of the informal trade made sure that nobody was left dry by the regulations. Unprecedented prices were achieved with mass increasing as well. The motivation was beer. Due to the ease with which one can make it, and the availability of it, demand spiked. Although the demand (price) dropped off after the ban on alcohol was lifted, it spiked immediately after the subsequent enforcement around week 29.

Garlic

The other product is garlic. Due to its medicinal qualities, garlic was seen as a potential remedy and as can be seen from the graphs below, increased significantly in price. Not all garlic is locally produced, and disruptions in supply further fuelled the prices.

In conclusion

South Africa has a strong agricultural sector. But its ability to support food security should not be confused with its size. Yes, we produce wonderful export products like fruit, wine, maize, soya. How do we harness this strength to strengthen local food security? We should not loose focus because we cannot not eat.

A discussion on this topic was held as a virtual meeting on 13 August 2020. The following points summarise the outcome of the exchange between participants.

- Trading food is one of the oldest activities and has been practiced over many generations over time. Processes are entrenched and attitudes are conservative.

- Many processes on fresh markets are not technology based but work well for participants in the value chain

- A systems approach to food chains is essential.

- Technology is not always the first solution, but smart processes and thinking are required.

- The food chain is really fragile. Its logistics complexity makes it even more so.

- Digital trade routes will eventually replace physical logistics.

- Getting product to users in smart ways will become the norm.

- The choice should always be with the consumer – no one can really dictate what people should eat.

- The role of food and culture should never be disconnected.

- Food safety is as important as food security

- Different relationships between producer and consumer exists, influencing the value chain. Some foodstuffs such as dairy cannot be distributed without regulation from a food safety point of view.

- In some cases, economies of scale my remain more effective than small scale or individual transactions.

- Historic location of food processing plants determined by legacy decisions makes food either inaccessible or very expensive.

- Clever use of primary food processing by-products may reduce the price and increase the nutritional value.

- Large food producers may deliver directly two small customers such as spaza shops and street vendors, making value chains shorter and more networked.

- In many cases a direct link between farmer and consumer may not be possible.

- It is important to have stratified system thinking and not only be very analytical.

- How we think about what we are dealing with will determine what we get.

- Food systems contribute to a complex subject and inside-out views are often followed instead of an outside-in approach giving voice to the consumer.

- Problems are easier to identify than to arrive at creative solutions, we often over-analyse instead of doing.

- People focus on not feeling hungry rather than eating right, focus is on calories rather than long-term health.

- Certain technologies like GIS are ideal to provide levels of information for small scale gardening and farming.

- Indigenous foods, such as insects, may hold large potential in a nutritional food chain.

- Value chains should not be addressed in isolation, but the whole economic system should be challenged, including existing practices. Standing back and getting a new perspective is essential.

- The food industry can learn from how the financial industry transforms.

- Thinking around solutions should be unemotional and not too analytical.

- Understand the industry at ground level before real solutions are to be offered.

- Unprecedented incidents, such as COVID-19, stimulate new initiatives in community farming, using existing spaces and new delivery systems.

- Quality awareness, regardless of the economic level (formal/informal) of the industry remains a key driver for product and process adoption.

- There are several levels that require attention, e.g. fresh products direct to the consumer and processed food. Going forward, the whole basket must be considered, and packaging of an entire balanced basket must be addressed.

- Guard against fixing something that is not broken. Many existing processes are trusted and work well. However, technology could improve matters even for the unbanked and small-scale operators.

- Markets remain key to food distribution. Innovation will come from the consumers themselves.

- The role of culture in food is not recognised in the modern food chain.

- People have lost their relationship with food and are disconnected from food.

- No individual can control food security, it is dependent on the system. This means that we have allowed food security to be contracted out to someone else.

- It must be clear who’s problem food security is and where responsibilities lie.

- The principle of relationship is important. We have to understand our relationship with food individually and collectively and have respect for that relationship in other cultures or communities. This depends on our relationship with ourselves and other people.

References

COVID-19, 2020. Dokumenter: Covid-19 inperking in samewerking met Helpende Hand en AfriForum. Youtube.com.

Du Plessis, A. 2020. Foodforward SA, 08 April 2020 – ENCA. Youtube.com.

Pierri, F. 2019. FAO SOUTH AFRICA – ENCA 13 July 2019. Youtube.com.

StatsSa, 2019. Towards measuring the extent of food security in South Africa. Statistics South Africa.

Dr Justy Range has an interest in all things technology, in how these “things” work and relate to us as humans. He currently works in the business development field, specifically focussing on solving value chain related problems in agriculture.

Mobile +27 83 324 7560 | email: justy@freshmarksystems.co.za